A recent quick-scan on the price formation in the value chain for tomato and lemon, followed by a workshop with relevant stakeholders, resulted in a clear path for change.

High-end supermarket (left) - informal logistics and open-air display of product at the central market (right)

Quick-scan

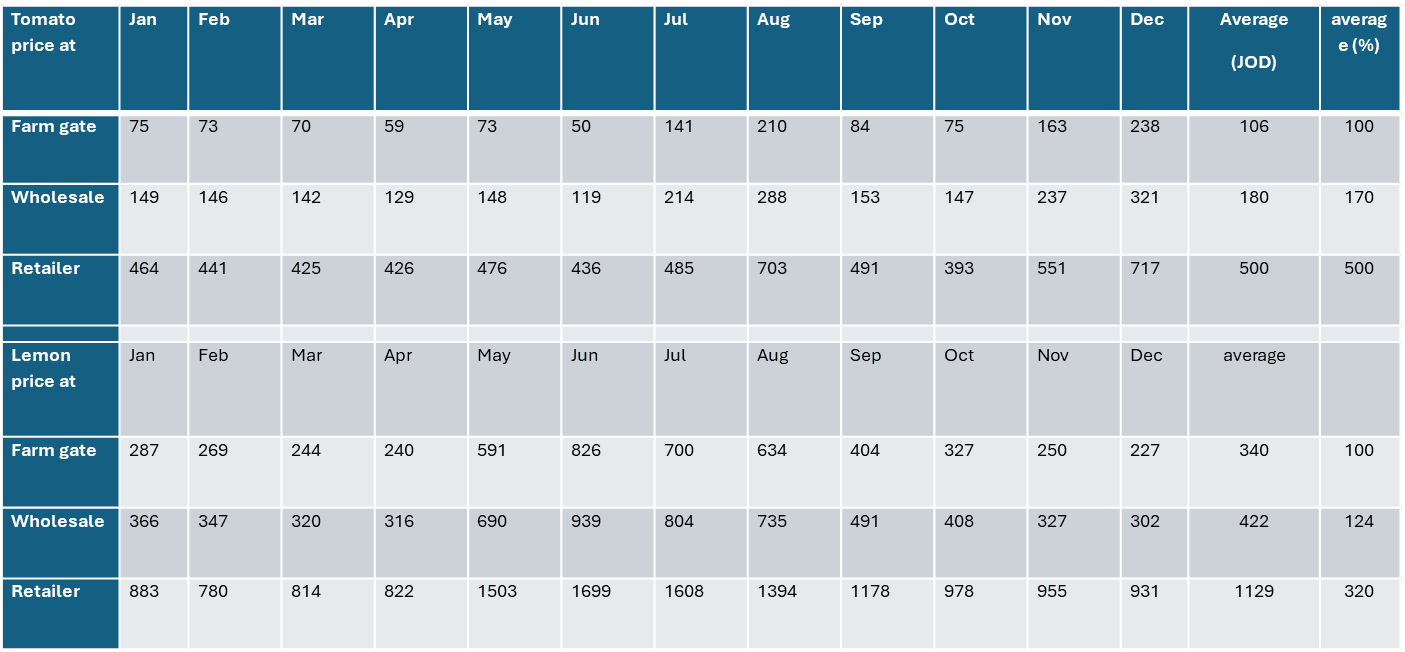

Over the past two years the LAN-team at the embassy in Amman has engaged with government and the private sector on policy-dialogue. Through a number of sessions, we discussed ways forward for food system roadmap, cooperative development and the role of the central market. To get the discussion to a very tangible, concrete level, we looked at the price-development in two value chains: that of tomato and of lemon. We used centrally, recently published data to understand the price formation throughout the year by analyzing the prices at Farm-gate, Wholesale and Retail (Table 1).

The price formation shown big differences throughout the year in absolute terms, while the mark-up is relatively stable percentage wise. The relative mark-up changes most for tomato from farm-gate to wholesale, with lowest in December (135%) and highest in October (232 %). Between the wholesale price and retail price is a relatively steady average mark-up of 300% for tomatoes and 200% for lemon.

Table 1. Monthly prices of tomato and lemon for 2024 at farm gate, wholesale market, and retail (JOD per ton)

Source: Department of Statistics, July 2025

Workshop:

The workshop for this public-private policy dialogue had representation from the Amman Central Market, the ministry of Agriculture, traders, brokers, the Jordan Cooperative Counsel and cooperatives themselves.

To the participants in this workshop, the scan raised the question of what justifies the high price increase between wholesale and retail – especially for tomato.

During the event we worked towards a common understanding of the logistical process and the prices setting mechanisms as well as the technical and organizational/ governance challenges in the current supply chain.

In the discission we realized that, before starting a ‘blame game’ on acceptable margins, we should look at what causes prices to increase during the value chain – the value addition and unnecessary cost-addition.

We then zoomed in on the key Costs-additions in the value chain – aspects that increase the price, without adding value, and found:

1- High losses and much labour required throughout the chain and at site of retail for continued sorting and grading due to:

- Short shelf-life due to poor varieties and inferior cultivation techniques (fertilizer use, irrigation, general plant health)

- Poor packaging material and -practices

- Informal logistics and infrastructure – for example the hand-held carts at the central market.

2- Cost-adding practices and market imbalance:

- Sorting and grading late in the value chain. In the value chain product of different grades are often mixed, with best product on top and lower grades on the bottom - with the idea of ‘fooling the buyer’ (see photos of pepper and tomato below). This results in added costs for sorting later in the chain.

- Inefficient sales process – brokers offer their produce in batches while waiting for buyers, while buyers search the market for best deals – product by product (see photo below)

- Storable produce, like citrus and to a lesser extend pepper, gives much room for speculation, while not adding value to the product. Generally, speculation adds risk (non-sales, quality reduction, cost addition for storage) and is (therefore) not a profitable strategy on the long run.

- Onward sales by buyers and traders are officially not accepted, but in practice a regular part of a sales process.

3- Market imbalance:

- In-transparent price formation, whereby large players generally have a good overview of the current prices from farmgate to retail, while smaller farmers and brokers are at a strong disadvantage.

- Due to low availability and/or access to market data farmers respond heavily to recent prices – high prices one year, quickly lead to over-production in the next. Jordan regularly experiences the ‘pig-cycle’ in parts of its agricultural production.

At the Central Market: lower quality produce gets hidden under higher quality produce, leading to extra costs for sorting later in the value chain (left.) Inefficient sales process – pop-up ‘auction’-type sale of a consignment of tomato (right).

(many, but achievable) Steps ahead:

This workshop created a clear awareness on how inefficiencies in the value chain led to unnecessary high prices for consumers, and inability for farmers to get a larger share of the end-price. And the awareness that quite of few of these inefficiencies are very much within reach of the stakeholders at the start of the supply chain.

Quick fixes seem to be 1) introducing Quality Standards for grading and food safety (and quality-control inspectors to enforce it at the central market and in the value chain), 2) a transition to quality of packaging material and 3) centralized data on market sizes and daily price-formation (national and for relevant international markets).

A bit further a-field are:

- Extension services for farmers to help them in the pre-harvest phase to increase shelf life (varieties, cultivation practices)

- cooled storage capacity and cooled logistics (internal logistics at the hub, collection transport, distribution),

- Electronic sales platform (auction) to overcome the laborious sales process

- Processing capacity of over-production (though over-production should remain limited when more market-information becomes available!)

These activities require clear investment plans and business cases but have been identified as part of the support work and the current governmental intervention strategies.

Workshop participants – Private sector and Government

Finally, farmers can take control of their own situation through Branding. Much can be said about how to introduce a successful brand. During the workshop a few key-interventions for the Jordan context were mentioned: create sufficient aggregation of product through cooperatives, establish an internal collective quality-standard and collaborate in value chains to reach the required access to market. Initiatives will need support in taking steps towards a good brand. Fortunately, such support is available through programs like Holland Horti Support and REGEP.

Please read the full report here.