Where do Ghana's vegetable farmers actually get their seed? And how do they decide what to plant? The answer runs well beyond imported varieties sold through agro-input shops, to seed saved on the farm and bought in local markets. Yet, comprehensive data on how vegetable farmers source seed have been lacking.

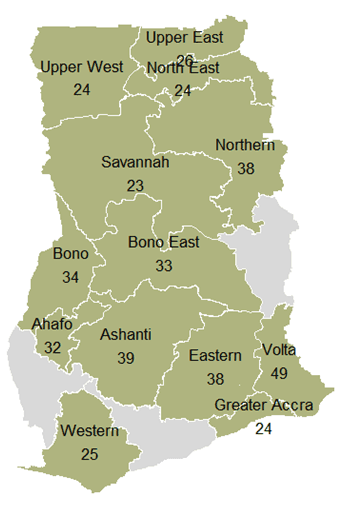

As part of the Ghana Seed Partnership, a nationwide study was conducted to document vegetable seed sourcing practices. Led by Advance Consulting, with fieldwork by the Ghanaian research firm Participatory Development Associates, the study interviewed 409 vegetable farmers across thirteen regions, 53 agro-input shops and 20 seed importers and distributors. Because respondents in twelve of the thirteen regions were sampled randomly, the results can be read as broadly representative of vegetable farming in Ghana. That makes the findings relevant well beyond the Partnership itself: for Ghanaian policymakers shaping the seed regulatory environment, for researchers, for seed companies, and for donors designing interventions in this space.

Farmer survey coverage

A smallholder sector with a threefold profit gap

Vegetable growing in Ghana is overwhelmingly a smallholder and commercial activity. The average farm in the sample measures 5.1 acres, of which 2.1 acres are planted with vegetables; pepper, tomato, okra and garden eggs dominate the fields. On their main crop, 56% of farmers use farmer-saved seed, 20% purchased open-pollinated varieties (OPV) and 24% F1 hybrid seed.

Vegetables grown, % of respondents

The economic rationale behind these choices are striking. Farmers using hybrid seed on their main crop report a median profit of around 6,350 GHS per acre, roughly three times the returns reported by farmer-saved seed users (2,256 GHS) and OPV users (1,776 GHS). Interestingly, the downside risk is similar across all seed types: in every group about a quarter of farms failed to break even. Hybrid seed thus raises the income ceiling without lowering the floor.

Access is unequal, most visibly by gender

The study reveals a marked gender gap: 47% of male-owned farms use hybrid seed on at least one crop, against only 15% of female-owned farms. Correspondingly, male-owned farms report a median profit of 3,348 GHS per acre, almost three times the 1,167 GHS on female-owned farms. Field observations suggest the gap is driven less by awareness or preference than by cost and access: women, who typically farm smaller plots, rely on farmer-saved seed because it is affordable, familiar and easy to obtain. Reaching women and cash-constrained smallholders will therefore depend on improving affordability and access, not on raising awareness alone.

A distribution chain built on trust, but short on credit

Agro-input dealers are the single most important sales channel, used by 51% of farmers. Yet own-saved seed and local markets remain major sources, especially in the Bono, Eastern, Northern and Western regions. Farmers are remarkably discerning: 43% of those buying from a dealer bypass the nearest shop to reach a preferred one, citing seed quality and trust as the main reasons. Trade credit, meanwhile, is thin along the entire chain: only 10–17% of dealers buy seed on credit, and just 13% extend credit to farmers. High seed costs, transport costs, poor roads and inadequate storage recur as challenges at every step, from importers losing entire shipments on bad roads to dealers unable to keep seed viable. Reliability matters too: when a farmer's preferred hybrid or OPV seed is out of stock, 79% fall back to farmer-saved seed, and none trade up.

Source of buying seeds, by region, % of respondents

Perception: convinced of the upside, confused about the product

Among the 63% of farmers who have heard of hybrid seed, perception is broadly positive: 90% believe it can raise income and 88% that it delivers better-quality produce, while satisfaction among actual users is near-universal (99% would replant, 98% would recommend it). At the same time, misconceptions persist: 64% believe hybrid seed is produced in a laboratory, 51% that it is genetically modified, and 22% that it is unsafe for human consumption. The dominant reason for non-use is not rejection but information: 68% of non-users simply say they do not know enough about it. And when farmers do form an opinion, they listen above all to fellow farmers (41%), far ahead of radio (8%), demonstration fields (6%) or social media (3%).

About the Ghana Seed Partnership

The Ghana Seed Partnership (GSP) was officially launched in October 2025 and will run up till June 2029. Funded by the Embassy of the Kingdom of the Netherlands, it brings together thirteen organisations from the Ghanaian and Dutch seed sectors, as expanded upon in article Ghana Seed Partnership: Strengthening Ghana - Netherlands Collaboration in Agribusiness. The Partnership works through four reinforcing work packages: improving the enabling and regulatory environment, establishing Ghana's first commercial vegetable seedling nursery, conducting variety trials, and developing the market for improved and hybrid varieties. The study presented here is a cornerstone of that fourth work package: it provides the evidence base for the Partnership's interventions and for a forthcoming campaign promoting improved varieties, and aligns with the Government of Ghana's own agenda to modernise the national seed system under the Feed Ghana Programme.

The full report, 'Demand, Distribution and Supply in Ghana's Vegetable Seed System', can be downloaded using this link.

More information

If you would like to know more, please send us an email via acc-lvvn@minbuza.nl.