The agricultural potential of Colombia is, without a doubt, enormous. However, it is not yet fully exploited. Meanwhile, Colombian cities steadily grow both in size and population, demanding agricultural production of higher quality and quantity. With this, comes to need for an efficient set of infrastructure and logistics operations, both for domestic and international trade.

Commissioned by the Embassy of the Kingdom of the Netherlands in Colombia, Resilience BV conducted a study aimed to analyse and present the current situation and bottlenecks of the agro-logistics sector in the five Caribbean departments of Atlántico, Bolívar, Cesar, La Guajira and Magdalena, as well as to identify business opportunities for (Dutch) investors that could help solve them. On the 7th of December at 16:00 CET (10:00 Colombian time) the results of this study will be presented during a webinar organised by the Embassy of the Kingdom of the Netherlands in Colombia, the Dutch-Colombian Chamber of Commerce – Holland House Colombia, and the logistics sector association of the Netherlands – Nederland Distributieland (NDL). After the presentation Dutch entrepreneurs active in Colombia will share their experiences related to agrologistics and doing business in the country.

We invite you to join us by registering on the following link: https://share.hsforms.com/1UQu-8rKYRretIhj1zpD99w4w6nv

Beeld: © LAN / LNV

Likewise, this year WUR conducted a sector study of agro-logistics in the Netherlands. This study aimed at identifying a working definition of the sector, describing ‘the ecosystem and international ambitions of Dutch agro-logistics companies’. This led the way to the creation of the so-called Dutch agro-logistics proposition, supported by NDL and Topsectors Agri & Food and Logistics, to be rolled out in different countries, including Colombia.

The momentum created by these studies reflects the growing interest and ambitions of the Netherlands to further strengthen (commercial) relations with Colombia, a crucial supplier for the Netherlands and Europe, by stimulating innovation and investment in the Colombian agro-logistics sector.

Insufficient local production: The reflection of challenges as well as growing demand

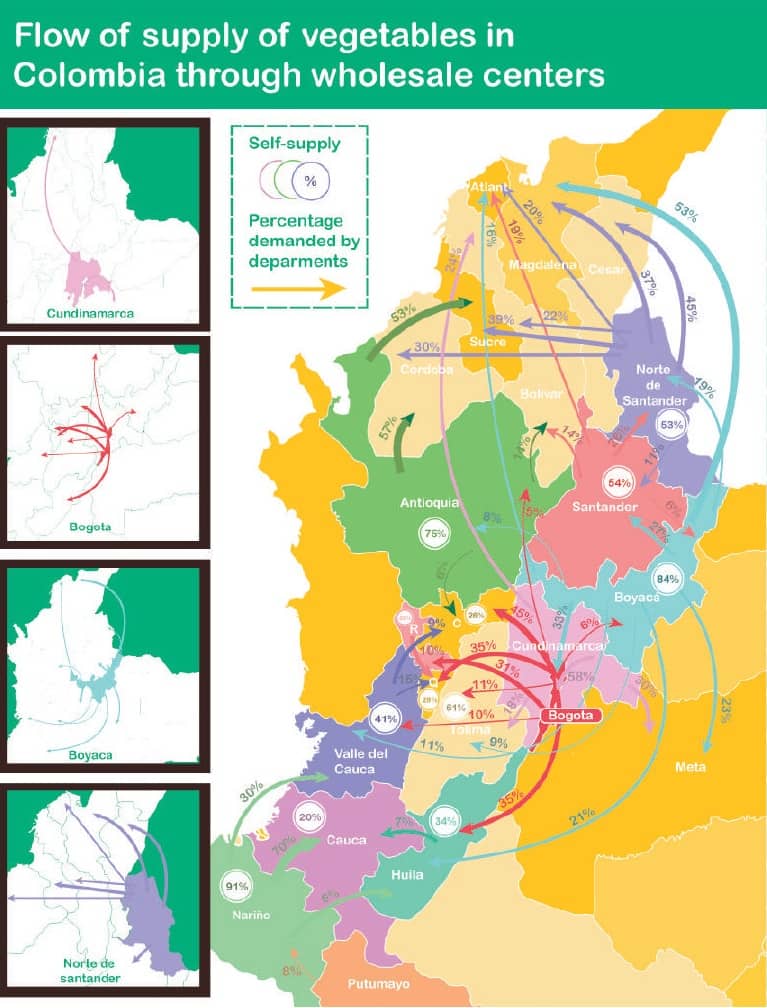

The five regions focus of the study are home to large production of banana and oil palm, largely destined to export markets. Other notable productions are cassava, rice, maize, plantain, and mango. Despite their overall suitable environmental conditions, most of the food consumed locally is not produced in these regions but transported from other departments with larger and more advanced agricultural production. Agricultural goods are transported to the wholesale markets of Granabastos and Mercabastos in Barranquilla (Atlántico) and Valledupar (Cesar), from where they are redistributed along the region. In the case of Granabastos, up to 90% of the products commercialized come from Santander, Valle del Cauca and the Cundinamarca-Boyacá highlands. In La Guajira, around 60% of the fruit and vegetables sold also comes from Santander.

Beeld: Taste the Future report (2020)

LAN Bogota

Amongst the main bottlenecks directly affecting growers are limited knowledge (technical and business), low formality and associativity and high input costs. Small and medium-sized producers are the ones experiencing lowest levels of technification, at times also lamenting low levels of technical assistance. While some (traditional) producers are reluctant to change and not interested in pursuing innovation, many simply do not have enough resources to improve their operations or are hesitant to adopt innovations and carry the risks of being the frontrunners. Similarly, producers often lack market and entrepreneurial knowledge, hindering the growth of their business and not allowing them to capture the entirety of the value they produce. These dynamics are certainly worsened by the low levels of formality and associativity: despite the presence of farmers’ cooperatives and associations, not all producers are eager to partake. Associations’ position is, in consequence, weakened in terms of negotiation and market access, limiting their appeal to potential members and partners, in what seems to be a vicious cycle. Unsurprisingly, all regions complain about the high costs of agricultural input. On top of the global fertilizers shortage caused in large part by the Russian-Ukrainian conflict, the situation has been aggravated in the last months by the depreciation of the Colombian Peso, posing serious risks for the survival of (especially small-scale) agricultural production of Colombia. Last but not least, limited access to finance poses a barrier for farmers to invest in their operations and production. This prevents them to access and adopt technologies that could increase productivity and/or quality of the produce, and lower its environmental impact.

Time is money: a long journey from farm to table

On average in Colombia, 72.5% of rural areas are located at more than 3 hours from main cities. In the ‘producer to consumer’ phase, the issues lay in a too high number of intermediaries, bad state of (tertiary) roads, difficulty to reach farms, low availability and high costs of transport and consequent low or even lack of value capturing by producers. Most agricultural supply chains are characterized by the presence of one or more intermediaries. These traders act as middlemen between the farmer and the wholesaler or retailer, or even between the farmer and another trader. Since most farmers do not have own means of transportation, they must rely on these intermediaries, that facilitate transport from farm gate to markets. Due to the numerous risks (such as accidents or lootings) and high (transport) costs the intermediaries are bearing, they add a substantial margin on their sales prices. This creates a large gap between the farm gate price and the market price, often regarded as unfair to the farmers.

Slow motion: a country relying on wheels

The internal logistics and infrastructure of Colombia need improvements. The bad state of tertiary roads and the high price and low availability of transport options reduce farmers’ chances to bring their produce directly to markets. By having to rely on intermediaries, farmers are eventually prevented from capturing the whole value of their production and work, and to be able to invest in improvements and access to new markets possibilities. A handful of Dutch companies provide innovative road maintenance and construction technologies; however, they would have to deal with complex public tendering procedures for infrastructure upgrades, which can reveal difficult for a foreign party.

In terms of inter-regional distribution, fluvial transport of agricultural commodities is not developed, given the economic advantages only come into play when handling high volumes. Currently, transit time by river between Barranquilla and Barrancabermeja can go from 4 to 5 days, compared to the 1-2 days of land transport for the same route. Furthermore, fluvial ports lack infrastructure for the maintenance of cold chains, which in turn strongly limits demand for improvements of fluvial transport for agricultural products. Similarly, at the current conditions and existing extension in the country, railways transport is not an option for agricultural products, especially when perishable.

Export is challenging on all levels

High (and increasing) costs for small producers (incl. bureaucracy and implications), hence low value retention, and increased shipping costs (vs stable sales price) were identified as the main bottlenecks to export. To sell their produce abroad, farmers need to be certified by the competent authorities depending on the type of product, i.e. ICA and/or INVIMA. This implies, on top of the required documents to be handed in, that production and/or transformation infrastructures comply with certain requirements. Often, small producers simply do not have the resources to invest in the required infrastructure upgrades, resulting in them selling to an intermediary and losing part of the price premium paid for export products, which in turn makes it difficult to reinvest in improved infrastructure or techniques.

With no exceptions, the pandemic-led global logistics crisis affected Colombian imports and exports operations. The departments of Atlántico, Bolívar, Cesar, La Guajira, and Magdalena host three of the four main ports for Colombia, playing a crucial role in the foreign trade of the country. These ports however also struggle with internal coordination challenges. Ports and authorities often have difficulties coordinating the different inspections and bureaucratic operations needed, such as those from the anti-narcotic police, the ICA and the douane agency. Ports complain not only about the different availabilities and working hours of the several authorities in charge of inspections, but also that inspection protocols are often developed on a central level and do not consider the dynamics of the region and the port itself. In addition, inspections of agricultural goods lack standardization, with some of them being random inspections and some depending on the track record of exporters.

Colombia exports mainly to countries in Europe and North America. Although having a privileged position for exports towards the Caribbean islands, specifically in the case of the Dutch Antilles, the potential is not fully exploited as shipping to the islands is too expensive, mainly due to the very low volume of imports back to Colombia. Collaboration amongst buyers on each island could also be improved by, for instance, use of cargo consolidation, which Colombian comercializadoras themselves still need to master. Dutch players could have a role in sharing know-how and/or providing services and technologies for an efficient cargo consolidation.

If you want to know more about this project, please contact us via: BOG-LNV@minbuza.nl