In this agri newsletter for Slovakia we give you a summary of the EIT Food report on the impact of Covid-19 on the agrifood sector in Slovakia, an update about ASF and on increasing consumer prices.

Beeld: EIT Food

EIT Food published individual country reports from Eastern and Central Europe on the impact of Covid-19 on the agrifood sector. You can find a summary of the countryreport Slovakia here, the full report can be downloaded with the link under the article.

The Slovakian Agri-Food Industry: Key Trends and Characteristics before COVID-19

Agriculture accounts for approximately 2% of generated Gross Value Added (GVA) in the Slovakian economy, and employs around 2.8% of the workforce. The growth of gross value added in agriculture since 2005 was partially conditioned by a significant and continuous profiling of agricultural production towards less input-intensive production, to a large extent. In the case of crop production, there was a tendency to expand monocultures of wheat and rapeseed on the expense of more labour and capital intensive production, such as fruits and vegetables. In the case of animal production, there was a decline in pig breeding.

At the same time, the sector was undergoing structural transformation. The successors to the original, typically inefficient large cooperatives have gradually merged into larger companies with unified and coordinated management. Their strong economic background, a significant decrease in the number of employees, modernization of technology, relatively low and stable input prices in conjunction with subsidy support have contributed to the consolidation of their dominant position in the market. Although generally self-sufficient in primary agricultural commodities (grains, potatoes, sugar beets, hops, pork, poultry), the Slovak agricultural sector suffers from low productivity and diversity. This is coherent with the fact that recorded large growth in GVA since 2020 partially results from the methodological issues related to national account statistics. A big problem which Slovakia faces at the moment is a shrinking workforce, as young people do not show interest in pursuing a career in agriculture. The companies operating in the agri-food sector show signs of low productivity, innovativeness and poor adaptation to newest technologies.

Looking at contribution to the total gross value added generated in the economy, Slovakian food processing is not as large as this industry is in other CEE countries. The biggest share of total food production is in dairy production (18%), meat production (17%), brewing (8%), poultry production (8%) and confectionery-baking production (7%). Slovak food retail sector is saturated and relatively consolidated. The top three retail chains together account for 71% of the revenues. With growing disposable income, Slovaks have become more keen on dining out. Furthermore, increasing tourism has also benefited full service restaurants specifically.

Import-dependence related to the final demand components

Around 50% of the food and beverages consumed by households in Slovakia come from import. For goods from the crop and animal production sector and fishing and aquaculture sector these percentages are lower – 26% and 30% respectively (with average for CEE at 23% and 68%).

Imported final consumption expenditure by the government, which includes the value of goods and services purchased or produced by general government and directly supplied to private households for consumption purposes, is substantially higher in Slovakia than in the CEE average in food and beverages manufacturing sector (0.74 vs. 0.30 average). The dependence in both fish and aquaculture sector (0.32) and the crop and animal production sector (0.14) is lower than on average in the CEE region.

Export-intensity of the agri-food industry in Slovakia

Due to the liberalisation of trade on global markets, including the agri-food markets, export competitiveness has become increasingly important in ensuring long-term success of companies by contributing to creation of their competitive advantage.

Slovakia’s agri-food industry is one of the least export-intense agri-food industries in the CEE region – exports in crop and animal production stand for just 23% of the total output, 19% in the fish and aquaculture and 17% in food and beverages manufacturing.

Identified macro vulnerabilities

According to the EC, "Slovakia has seen significant economic growth in recent decades and has been catching up with the EU average, thanks to important reforms and structural changes that have taken place. As convergence with the EU weakens, population ageing, climate change and the digital transformation pose long-term challenges to the country’s economy and to fiscal sustainability."

In regards to the labor market, Slovakian trends are in line with regional trends – wages have increased steadily, above the increase of productivity. Worker shortages, also a CEE-wide phenomena, have led to large salary increases. While these increases improve living standards, they have had a negative effect on cost competitiveness.

Slovakian households are also charactized with low savings and increasing indebtedness. This is a potential vulnerability for further growth, as household debt has reached a record high of 42.8% of GDP in 2019, driven by rising housing prices and higher mortgages.

A further potential macro vulnerability is the lack of adequate education and training that would allow many students to improve the business environment in Slovakia, which is lacking local entrepreneurs. Issues also noted are long processes for permits and resolve insolvency, which hampers investment due to uncertainty in the regulatory process.

Beeld: EIT Food

COVID-19 Impact on the Agri-food industry in Slovakia

The most affected parts of the Agri-food industry value chain in Slovakia were food processing, transport and HoReCa sector (particularly restaurants). Agriculture mostly suffered from labour shortages, while other factors played a minor role. Consumer demand for food products managed to rise by 1% y/y and, after some fluctuations, rose by the same amount in July.

Like in other CEE countries, Slovakian agriculture is relatively resilient to the COVID-19 crisis and its further development will be more a function of structural factors, like EU Green Deal, smart specialization and economies of scale. In turn, manufacturing of foodstuffs in Slovakia is highly vulnerable to disturbances in global value chains due to the high share of imported goods (compared to CEE average). Food processing has also low export intensity, which might mitigate risks associated with international flows, but at the expense of a high reliance on small domestic demand. In the recession context, cheaper and basic products should perform better in terms of recorded sales.

Being the most affected by the pandemic, HoReCa sector is a significant source of demand for farmers and input providers. While the initial lockdown measures and containment shocks affected the two interlinked sectors negatively, following the reopening of borders, more local tourism could be an opportunity for the agricultural sector in the near future. As travel outside of the European Union continues to be filled with uncertainty, tourists from the EU may opt to travel more inside of union. Therefore, the pandemic offers a potential influx of more European tourists to the tourist destinations in Slovakia’s mountains.

Outcomes of the Scenario Analysis and Consequences

Agricultural & Input providers

- Agricultural and input providers are (of the three sectors evaluated) uniquely exposed to price shocks in global commodity markets. However, eurozone membership might alleviate this effect for Slovakia.

- Shifts to lower-value added produce (associated with the New consumer and Disruption scenarios) offer a potential opportunity in the form of slight demand boosts. This could require changing the past trend of expanding monoculture production.

- Seasonal labour disruptions are a distinct risk for this sector, with lockdowns applying strong wage pressure. In this case, too strong exchange rate of the euro could become a challenge.

- Consumers may increasingly pay greater attention to ingredients and preservatives added to raw or low-processed products, as a way to sustain good immunity

- Higher disruption might be expected for goods consumed mostly by those with lesser spending power, characterized by high sensitivity (elasticity) of the demand to changes in prices and disposable income. To a degree this supports demand for certain agricultural sectors, but not others. Livestock and higher end meat production may suffer in worse economic climates on account of price.

Food & Beverage Manufacturing

- Success and shape of food processing sector strongly tied to demand for high value-added products

- Significant source of demand for high value added produce depends on HoReCa sector as well as condition of the tourism sector in Slovakia

- Long-lasting contraction of tourism in Slovakia may translate into reduced opportunities for local value adding processing

- Lockdown impacts on restaurants to be modulated by delivery apps and stringency of policy

- Manufacturers benefit from global surpluses – capturing value from falling prices of inputs, on condition that currency rates stabilise as well as public policies will not largely influence prices.

Retail

- (Grocery) retailers better insulated from pandemic shocks than other sectors – shifts from restaurant consumption to home consumption supports consumption of groceries.

- Online grocery retail becomes a key medium for competition, requiring strong investment in logistical networks and online advertising structures. Hovewer, moderate urbanization of Slovakia might hamper growth of the digital channel.

- Shift to online grocery shopping risks reduction of traffic through brick-and-mortar stores, putting pressure on stores that may struggle to pay overheads. This effect will be rather limited to cities with a certain level of competition in retail trade.

- As a country with a significant tourism sector (regarded as strategically important to the economy, Slovakian retail (including HoReCa) is highly exposed to containment measure risks.

- In a New Rulebook scenario, structurally, consumers revert to demand for similar produce as consumed before the pandemic, however restrictions reduce the scale of total consumption.

- In the event of favourable economic conditions, consumer confidence and spending power will recover and grow, allowing the market to return to pre-pandemic trends of growing demand for higher quality and higher value added goods.

- Demographic changes may impact sales. Reports suggest during lockdowns, men increasingly take over the role of primary grocery buyer for households, with retailers reporting consequent changes to what is bought and how.

Beeld: © Richard Knol / Richard Knol

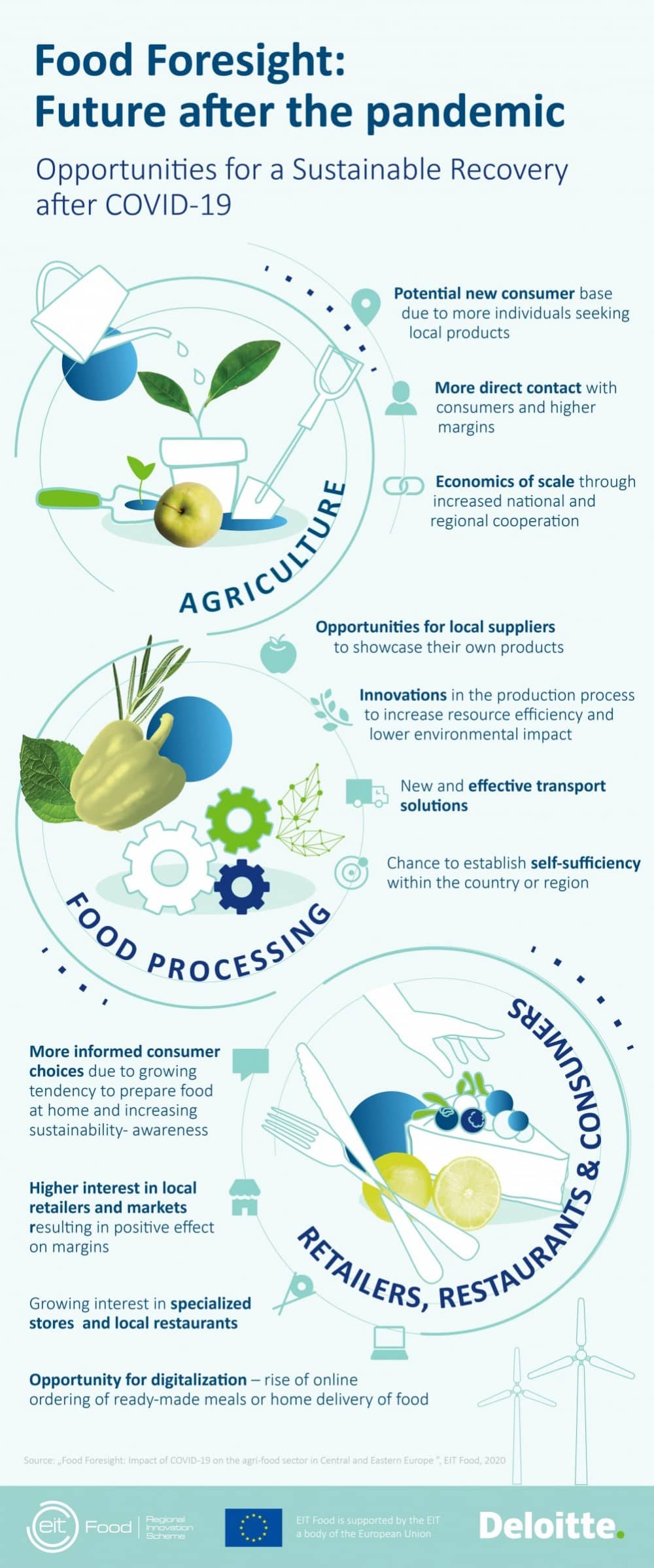

Key Opportunities for a Sustainable Recovery

Farmers and input providers

|

Oportunity |

Source |

|

Potential new consumer base |

More individuals seeking local products |

|

Innovations in the production process towards better resource efficiency and lower environmental impact |

Changing demand and social preferences requiring alterations to the production process |

|

More direct contact with consumers and higher margins |

Shortened distance between farmers and consumers as a result of changing consumer preferences |

|

Economies of scale through increased national and regional cooperation |

Disruption of larger international supply chains but continued investments in transport infrastructure in CEE |

Food processing, storage, and transport

|

Oportunity |

Source |

|

Opportunities for local suppliers to showcase their own products |

Growing consumer interest in local goods as well as products will lower environmental footprint |

|

Opportunity to “green” the food production process |

Changing demand requiring alterations to the production process |

|

New and effective transport and storage solutions |

Transport disruptions |

|

Need for higher self-sufficiency within the country or region |

Trade and supply chain disruptions |

Retailers, restaurants, and consumers

|

Oportunity |

Source |

|

More informed consumer choices and new fields of competition |

Growing tendency to prepare food at home and sustainability-awareness |

|

Higher interest in local food retailers and markets and resulting positive effect on margins |

Growing consumer interest in local products |

|

Growing interest in specialized stores and resulting positive effect on margins |

More demanding consumers due to continued socio-economic development or health & dietary needs |

|

Digitalization – rise of online ordering and home delivery of food |

Necessity or desire to remain home |

For the full report and the individual reports of other countries in Central and Eastern Europe:

Beeld: © A. Galica

African swine fever has spread to the ninth district

During the 16 months of the presence of African swine fever (ASF) in the territory of the Slovak Republic, the disease spread to the ninth district. The district of Bardejov was added to the districts of Trebišov, Michalovce, Košice-okolie, Košice-mesto, Rožňava, Rimavská Sobota, Vranov nad Topľou and Prešov. In total, Slovakia has registered 342 cases of ASF in wild boars and 28 outbreaks in domestic pigs during this period.

On November 6, 2020, the National Reference Laboratory in Zvolen confirmed a positive result for ASF in 2 wild boars in the cadaster of the municipality of Nižné Raslavice in the Bardejov District. This is the first confirmation of the occurrence of the disease in the area.

The relevant Regional Veterinary and Food Administration of Bardejov will issue measures for the defined hunting grounds in accordance with the valid legislation of the EU and the Slovak Republic, which are to prevent further spread of the disease resp. ensure that it slows down.

In Slovakia, hunters were ordered to intensively hunt wild game, to which hunters responded responsibly. The Ministry of Agriculture and Rural Development of the Slovak Republic (MPRV SR) enabled hunters to hunt wild game all year round, regardless of gender and age. There is also an active monitoring of the situation by state veterinarians and hunters, to whom the state reimburses the costs of sampled samples from found and caught wild boar. The submitted samples are constantly examined in the veterinary laboratory in Zvolen.

According to the ministry, the incidence of ASF in neighboring countries is deteriorating, so the real threat of further findings has far from disappeared and will not disappear, especially if everyone, from small farmers to breeders, hunters and ordinary citizens, does not behave responsibly and does not respect veterinary measures. The handling of fodder, from mown maize to straw, which can be infected, is also important.

The further development of the disease in Slovakia will be decided by the responsible approach of the stakeholders. The MPRV SR therefore calls for extreme caution.

Source: https://www.mpsr.sk/sk/

Beeld: NL embassy PL

Consumer prices started growing again

More expensive vegetable, bread and non-alcoholic beverages pushed prices up. After seven months of a decreasing inflation rate, mild growth was noticed in consumer prices.

The prices of goods and services increased 1.6 percent year-on-year in October 2020, up 0.2 percentage points compared with August and September, when the annual inflation reached 1.4 percent, according to the Statistics Office data.

Still, the October inflation is the second lowest in the recent three years.

Prices in hospitality sector up

Higher prices in restaurants and hotels in particular, as well as in health care, influenced the development despite the coronavirus crisis. On the other hand, the development of prices in transport and the decrease of prices of alcoholic beverages prevented the further growth of inflation.

The prices in restaurants and hotels were the biggest to grow in y-o-y comparison, by 4.2 percent. The prices of various goods and service went up 4.1 percent, health care by 3.8 percent, education by 2.9 percent, living, water, electricity, gas and other fuels by 2.5 percent, groceries and non-alcoholic drinks by 1 percent.

Only prices in transport dropped by 4.6 percent, postal services remaining at the same price.

Prices increased by 0.1 percent in monthly terms, especially that of groceries. They rose 0.3 percent m-o-m after a four-month drop. More expensive vegetables, bread and non-alcoholic beverages pushed prices up.

Expected growth

The acceleration in the inflation rate was expected, according to Ľubomír Koršňák, analyst of the UniCredit Bank Czech Republic and Slovakia.

Sádovská expects that the prices of goods and services will be increasing in the coming months, oscillating between 1 and 2 percent y-o-y. She does not expect deflation.

Also Koršňák expects inflation to account for some 1.5 percent. At the beginning of next year, we will possibly see another drop in the inflation tempo, to 1 percent, he summed up.

Source: Slovak Spektator